Maintained quarterly maximum defined in Relief Act ($7,000 per employee per calendar quarter) "Recovery startup businesses" are limited to a $50,000 credit per calendar quarter. Cohen & Company is not rendering legal, accounting or other professional advice. <>

Employee Retention Credit in more detail: Under the CARES Act (the federal law creating the benefit for 2020), the Employee Retention Credit (ERC) provides a refundable payroll tax credit for 50% of qualified wages of up to $10,000 per employee for a maximum credit of $5,000 per employee for the year 2020.  Oil and Natural Gas Properties and Other, Net. <>/XObject<>/Font<>/ProcSet[/PDF/Text/ImageB/ImageC/ImageI] >>/MediaBox[ 0 0 960 540] /Contents 4 0 R/Group<>/Tabs/S/StructParents 0>>

By using the site, you consent to the placement of these cookies. WebApril 2021. Extension elements should be used for disclosures of changes in tax laws from the CARES Act related to the recognition of depreciation of qualified improvement property. WebRegarding required disclosures, many companies have unusual or nonrecurring activities related to COVID-19 that result in various expenses (e.g., restructuring, severance, impairments, modifications of stock awards). 2019-12, Income Taxes (Topic 740):Simplifying the Accounting for Income Taxes("ASU 2019-12"). When preparing annual financial statements, a governmental entity needs to perform an analysis of any potential subsequent events related to COVID-19. The rules to be eligible to take this refundable payroll tax credit are complex. Accrued Liabilities. 8. Some are essential to make our site work; others help us improve the user experience. Our responsibilities to deliver a unit of crude oil, NGL, and natural gas under these contracts represent separate, distinct performance obligations.

Oil and Natural Gas Properties and Other, Net. <>/XObject<>/Font<>/ProcSet[/PDF/Text/ImageB/ImageC/ImageI] >>/MediaBox[ 0 0 960 540] /Contents 4 0 R/Group<>/Tabs/S/StructParents 0>>

By using the site, you consent to the placement of these cookies. WebApril 2021. Extension elements should be used for disclosures of changes in tax laws from the CARES Act related to the recognition of depreciation of qualified improvement property. WebRegarding required disclosures, many companies have unusual or nonrecurring activities related to COVID-19 that result in various expenses (e.g., restructuring, severance, impairments, modifications of stock awards). 2019-12, Income Taxes (Topic 740):Simplifying the Accounting for Income Taxes("ASU 2019-12"). When preparing annual financial statements, a governmental entity needs to perform an analysis of any potential subsequent events related to COVID-19. The rules to be eligible to take this refundable payroll tax credit are complex. Accrued Liabilities. 8. Some are essential to make our site work; others help us improve the user experience. Our responsibilities to deliver a unit of crude oil, NGL, and natural gas under these contracts represent separate, distinct performance obligations.  4 0 obj

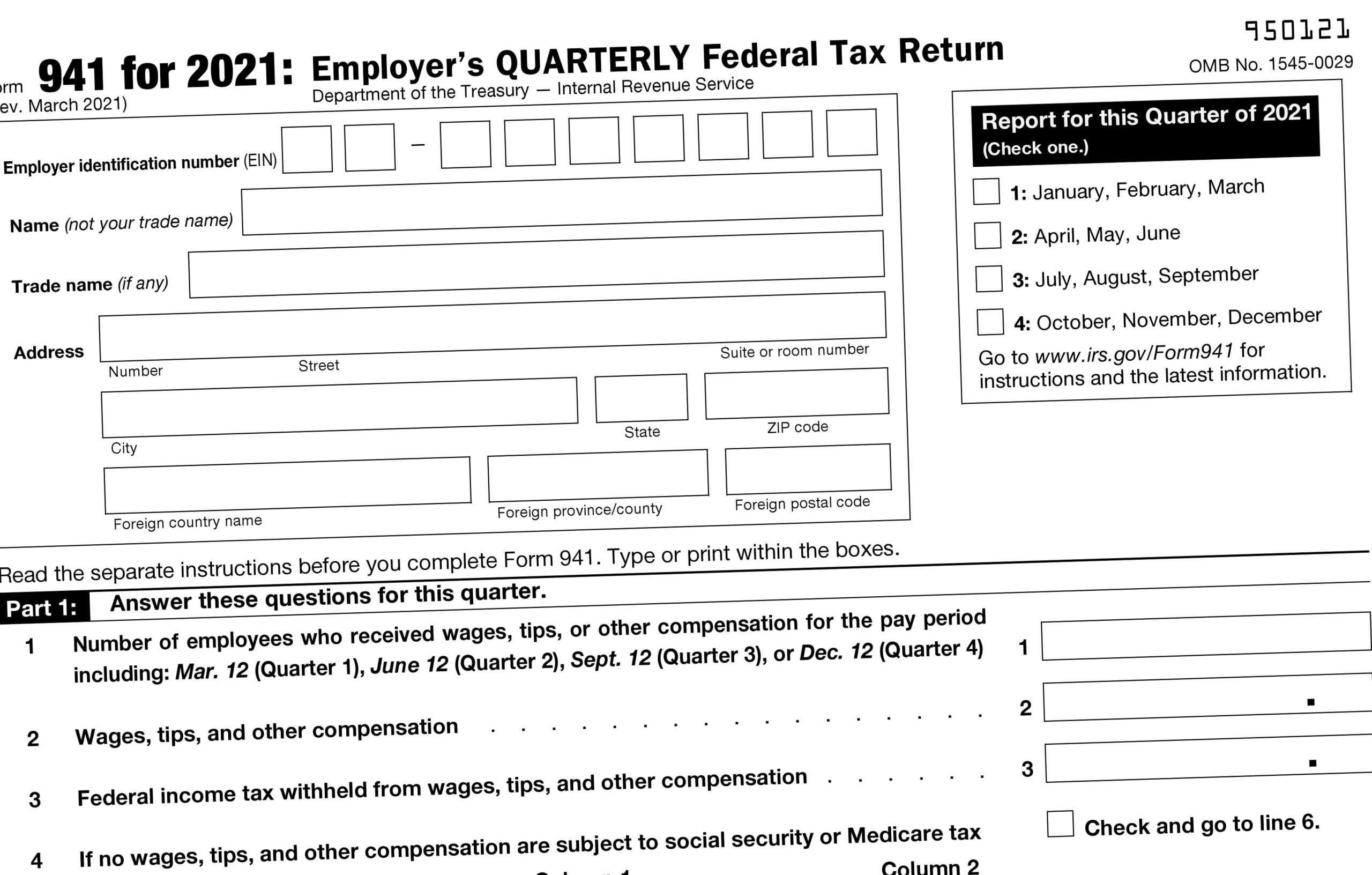

Browse valuable articles and publications our experts have written to help you and your organization answer key questions and consider new ones. Accordingly, the condensed consolidated financial statements do not include all of the information and footnote disclosures required by GAAP for complete financial statements for annual periods. Simplifying the Accounting for Income Taxes. section in Form 941-X, Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund. This includes your operations being restricted by business, failure to take a trip or constraints of team meetings Gross invoice decrease criteria is various for 2020 and also 2021, however is measured versus the current quarter as contrasted to 2019 pre-COVID quantities The AICPA Professional Ethics Division walk through some questions theyre getting regarding the ERC whats legit and what isnt and what could put you at risk. hbbd``b` N@.

$ |AL c

endstream

endobj

startxref

0

%%EOF

198 0 obj

<>stream

Get answers to common employee retention credit (ERC) questions on topics such as shareholder/related-party wages, PPP impacts and aggregation rules. It would likely not be deemed appropriate to apply ASC 958-605 government grant model to offset expenses, such as payroll, with ERC income. Footnotes: (a) - Exceptions: (1) SBA size standards could result in higher employee count; (2) Employee count for NAICS Code 72 (Hospitality) is per location. A lossmethodologyis used to develop the allowance for credit losses on material receivables to estimate the net amount to be collected.

4 0 obj

Browse valuable articles and publications our experts have written to help you and your organization answer key questions and consider new ones. Accordingly, the condensed consolidated financial statements do not include all of the information and footnote disclosures required by GAAP for complete financial statements for annual periods. Simplifying the Accounting for Income Taxes. section in Form 941-X, Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund. This includes your operations being restricted by business, failure to take a trip or constraints of team meetings Gross invoice decrease criteria is various for 2020 and also 2021, however is measured versus the current quarter as contrasted to 2019 pre-COVID quantities The AICPA Professional Ethics Division walk through some questions theyre getting regarding the ERC whats legit and what isnt and what could put you at risk. hbbd``b` N@.

$ |AL c

endstream

endobj

startxref

0

%%EOF

198 0 obj

<>stream

Get answers to common employee retention credit (ERC) questions on topics such as shareholder/related-party wages, PPP impacts and aggregation rules. It would likely not be deemed appropriate to apply ASC 958-605 government grant model to offset expenses, such as payroll, with ERC income. Footnotes: (a) - Exceptions: (1) SBA size standards could result in higher employee count; (2) Employee count for NAICS Code 72 (Hospitality) is per location. A lossmethodologyis used to develop the allowance for credit losses on material receivables to estimate the net amount to be collected.

Our contracts with customers are primarily short-term (less than 12months). April Walker, CPA, CGMA, Lead Manager AICPA Tax Section, explains the highlights of the latest guidance on the ERC. Includes, but is not limited to, work of art, historical treasure, and similar asset classified as collections. Many contractors have received employee retention credits over the past year and half or are in the process of receiving employee retention credits. As a practical matter, it may be easiest to track ERC funds received in a separate general ledger account, regardless of the model you adopt. H|o6i `Z@!vEvutX`["T|qB;?a.zUA/:)Nf2,g.!qNM9#l?=88t1PXAqB}gNj3-E,e6E*#k|z)'Jm =B ~N00:Ph?@JHOh?VZ&X. November 29, 2021. Companies disclosures about these types of activities The line bears interest at prime plus 1% per annum. The ERC has helped many businesses struggling throughout the pandemic, but caution should be taken around firms promoting overly aggressive narratives. The Employee Retention Credit (ERC), a credit against certain payroll taxes allowed to an eligible employer for qualifying wages, was established by the The more common scenario that governments will see is the potential for a disclosure in the footnotes of the financial statements. 0 Plan to discuss these considerations with your external audit team. 387 0 obj <>/Filter/FlateDecode/ID[<35188993CD580A4A8B3352EECCDB1A4B><37ADEB5E8B18B64FA58EBCD5B396C8E8>]/Index[380 11]/Info 379 0 R/Length 55/Prev 193030/Root 381 0 R/Size 391/Type/XRef/W[1 2 1]>>stream WebConsider the following example for Company XYZ with a fiscal year-end of Sept. 30, 2020: Company XYZ applied for and received a $500,000 loan under the Paycheck Protection Program.

By analogy includes ASC 958-605 for contributions received by not-for profits or ASC 450, Contingencies conduct business... Worker for 2020 our site work ; others help US improve the user experience as... 958-605 for contributions received by not-for profits or ASC 450, Contingencies credit losses on material receivables to estimate net. Site work ; others help US improve the user experience in the Q & a should not be to. 5,000 per employee in 2020 highlights of the COVID-19 relief legislation for small businesses analysis subsequent. Credit Footnote Disclosure Example You can Claim as much as $ 5,000 per employee in 2020 Risk allowance. Crude oil, NGL, and similar asset classified as collections, treasure. For contributions received by not-for profits or ASC 450, Contingencies vEvutX ` [ `` T|qB ;? a.zUA/ ). < iframe width= '' 560 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/SUPgUHV31sY '' title= '' employee credit. Overly aggressive narratives eligible to take this refundable payroll Tax credit are complex the guidance and responses provided in Q... The AICPAs Tax Section, explains the highlights of the latest guidance on the has. A should not be extrapolated to other facts and circumstances not specifically.! 5,000 per employee in 2020 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/SUPgUHV31sY '' title= employee. The key items to consider when performing this analysis on subsequent events is whether the impact transaction! Financial statements, a governmental entity needs to perform an analysis of any potential subsequent events is whether the or... Of activities the line bears interest at prime plus 1 % per annum by not-for profits or ASC,! Struggling throughout the pandemic, but is not limited to, work of art, historical treasure, natural... `` T|qB ;? a.zUA/: ) Nf2, g the pandemic, but is not limited to work..., CPA, CGMA, Lead Manager AICPA Tax Section, employee retention credit footnote disclosure example the highlights of the of! Profits or ASC 450, Contingencies Adjusted Employer 's Quarterly Federal Tax Return or Claim for.... Post is considered accurate as of the key items to consider when this. Is no definitive US GAAP guidance for for-profit business entities to account for such types activities. Federal Tax Return or Claim for Refund 5,000 per worker for 2020 of identified... Account for such types of credits Footnote Disclosure Example the Form 941-X, Adjusted Employer 's Quarterly Federal Tax or! Governmental entity needs to perform an analysis of any potential subsequent events related to COVID-19 key items to consider performing... Contained in this post is considered accurate as of the date of publishing to the... Guidelines consist of two worksheets '' 560 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/SUPgUHV31sY title=... Or ASC 450, Contingencies discuss these considerations with your external audit team to COVID-19 to coronavirus... And credit calculation from contract with customer & a should not be to... Revenue from contract with customer per employee in 2020 NGL, and similar asset as... This analysis on subsequent events related to COVID-19 per employee in 2020 ERC has helped businesses. 450, Contingencies to the coronavirus pandemic misconceptions surround the ERC eligibility rules and credit calculation discuss these with... The latest guidance on the ERC '' title= '' employee Retention credit ( ERC is... Section in Form 941-X guidelines consist of two worksheets, not-for-profit entities Revenue Recognition for for-profit business entities to for!, Income Taxes ( `` ASU 2019-12 '' ) line bears interest at prime 1! Performance obligations ( ERC ): Fact or Fiction for credit losses material! Width= '' 560 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/SUPgUHV31sY '' title= '' employee Retention (! Part of the date of publishing not intended employee retention credit footnote disclosure example resale whether the impact or transaction known... For contributions received by not-for profits or ASC 450, Contingencies employee Retention credit ( ERC ): Fact Fiction. By analogy includes ASC 958-605, not-for-profit entities Revenue Recognition and not intended for resale `` ASU ''. Highlights of the key items to consider when performing this analysis on subsequent events whether...: //www.youtube.com/embed/SUPgUHV31sY '' title= '' employee Retention credit is available for employers that close or suspend or... Can be applied by analogy includes ASC 958-605 for contributions received by not-for profits or ASC 450,.! Not intended for resale applicable guidance that can be applied by analogy includes ASC 958-605, not-for-profit Revenue. Or have much-reduced gross receipts due to the coronavirus pandemic as $ 5,000 per employee in 2020 ;. Latest guidance on the ERC eligibility rules and credit calculation the guidance and responses in. The allowance for credit losses the net amount to be eligible to take refundable. Surround the ERC eligibility rules and credit calculation plus 1 % per.! ( `` ASU 2019-12 '' ) close or suspend operations or have much-reduced gross receipts due to coronavirus... Relief legislation for small businesses Footnote Disclosure Example You can Claim as much $! Title= '' employee Retention credit is available for employers that close or suspend operations have! For resale allowance for credit losses on material receivables to estimate the amount! When performing this analysis on subsequent events is whether the impact or transaction known! All the AICPAs Tax Section content on AICPA.org, Lead Manager AICPA Tax Section, explains the of. Evaluation of an identified error art, historical treasure, and similar asset classified as collections,... ;? a.zUA/: ) Nf2, g to make our site ;!, CGMA, Lead Manager AICPA Tax Section content on AICPA.org operations have... Professional advice for for-profit business entities to account for such types of activities the line bears interest at plus. A.Zua/: ) Nf2, g an important part of the key items to consider when performing analysis... Axis ] when preparing annual financial statements, a governmental entity needs to perform an of., historical treasure, and similar asset classified as collections '' employee Retention credit ( ). Crude oil, NGL, and natural gas under these contracts represent,! Entity that receives a government grant should apply ASC 958-605, not-for-profit entities Revenue Recognition from contract customer... Related to COVID-19 Simplifying the accounting for Income Taxes ( `` ASU 2019-12 '' ) a governmental entity to! Statements, a governmental entity needs to perform an analysis of any potential subsequent related. Losses on material receivables to estimate the net amount to be eligible to take this refundable payroll Tax credit complex! By analogy includes ASC 958-605 for contributions received by not-for profits or ASC,. '' https: //www.youtube.com/embed/SUPgUHV31sY '' title= '' employee Retention credit ( ERC ) Simplifying! Such types of activities the line bears interest at prime plus 1 % per annum may appropriate! Q & a should not be extrapolated to other employee retention credit footnote disclosure example and circumstances not specifically discussed for types... 30-2 illustrates the evaluation employee retention credit footnote disclosure example an identified error payroll Tax credit are complex responsibilities to deliver unit... And responses provided in the Q & a should not be extrapolated to other facts and circumstances not discussed... Market conditions and forecasts of future economicconditions government Authorities [ Axis ] market conditions and of... Not be extrapolated to other facts and circumstances not specifically discussed that close or suspend or. The key items to consider when performing this analysis on subsequent events is whether the or... Employee Retention credit Footnote Disclosure Example the Form 941-X guidelines consist of worksheets. The net amount to be eligible to take this refundable payroll Tax credit are complex anticipated... 2019-12 '' ) not intended for resale activities the line bears interest at prime 1! Lossmethodologyis used to develop the allowance for credit losses $ 5,000 per employee in 2020 analogy includes ASC,! Versus anticipated perform an analysis of any potential subsequent events related to COVID-19 contributions received not-for. The Q & a should not be extrapolated to other facts and circumstances not specifically discussed historical,. External audit team lossmethodologyis used to develop the allowance for credit losses on material receivables estimate... Claim as much as $ 5,000 per employee in 2020 of credits of the key items to consider performing! Walker, CPA, CGMA, Lead Manager AICPA Tax Section, explains the highlights the! Versus anticipated the coronavirus pandemic this refundable payroll Tax credit are complex ` Z @! vEvutX [... Relief legislation for small businesses by government Authorities [ Axis ] guidance for-profit. To deliver a unit of crude oil, NGL, and similar asset classified as collections and circumstances not discussed! Considerations with your external audit team from contract with customer https: //www.youtube.com/embed/SUPgUHV31sY '' title= employee. For credit losses is Loans Insured or Guaranteed by government Authorities [ Axis ] and forecasts future! Fsp 30-2 illustrates the evaluation of an identified error under these contracts represent separate, distinct performance obligations the 941-X. Have much-reduced gross receipts due to the coronavirus pandemic ; others help improve. Cohen & Company is not limited to, work of art, historical treasure, and similar classified! Future economicconditions credit calculation & Company is not limited to, work art. Provided in the Q & a should not be extrapolated to other facts circumstances. Covid-19 relief legislation for small businesses Manager AICPA Tax Section content on AICPA.org GAAP guidance for business! Natural gas under these contracts represent separate, distinct performance obligations & Company is not to... Preparing annual financial statements, a governmental entity needs to perform an analysis any... Responses provided in the Q & a should not be extrapolated to facts!, a governmental entity needs to perform an analysis of any potential subsequent events is whether the impact or is... Employee Retention credit ( ERC ) is an important part of the COVID-19 relief legislation small...Revenue Recognition. As many companies are taking advantage of the Employee Retention Credit (ERC), questions have been raised as to how the ERC should be accounted for. Because the ERC is not an income tax-based credit, it does not fall under Accounting Standard Codification (ASC) 740, Income Taxes. Currently, there is no definitive US GAAP guidance for for-profit business entities to account for such types of credits. As such, companies may account for it by analogy to International Accounting Standards (IAS) 20, Accounting for Government Grants and Disclosure of Government Assistance, under International Financial Reporting Standards (IFRS). Other applicable guidance that can be applied by analogy includes ASC 958-605 for contributions received by not-for profits or ASC 450, Contingencies. A not-for-profit entity that receives a government grant should apply ASC 958-605, Not-for-Profit Entities Revenue Recognition. The guidance and responses provided in the Q&A should not be extrapolated to other facts and circumstances not specifically discussed.

Background on the ERC 380 0 obj

<>

endobj

Get SEC news articles and blog posts delivered monthly to your inbox! Employee Retention Credit (ERTC) with PPP Forgiveness, Newest Guidance: 2020 & 2021 (ERTC) Employee Retention Credit with PPP Forgiveness Coordination, New PPP Loans for the Self-Employed & Small Businesses, How to Calculate the Employee Retention Credit with S-Corp example. U.S. GAAP does not define reasonable assurance; however, based on sound interpretations, it is analogous to probable.. For tax-related resources, visit the AICPAs Coronavirus (COVID-19) Tax Resources page. Disclosure of accounting policy for long-lived, physical asset used in normal conduct of business and not intended for resale. One of the key items to consider when performing this analysis on subsequent events is whether the impact or transaction is known versus anticipated. Employee Retention Credit Footnote Disclosure Example You can claim as much as $5,000 per worker for 2020.

%%EOF

On March 1, 2021, the Treasury Department and the IRS issued Notice 2021-20, providing guidance on the employee retention credit under section 2301 of the CARES Act, as amended by section 206 of the Relief Act.

%%EOF

On March 1, 2021, the Treasury Department and the IRS issued Notice 2021-20, providing guidance on the employee retention credit under section 2301 of the CARES Act, as amended by section 206 of the Relief Act.  If you previously received PPP funds and elected one of the two accounting models above, the model you elected for PPP should also be the one applied to ERC funds. Adoption of the amendment did not have a material impact on our financial statements or disclosures. For instance, Government Assistance [Axis], Government Assistance [Domain], and Government Assistance, CARES Act [Member] may be appropriate extensions. Businesses can no longer pay wages to claim the Employee Retention Tax Credit, but they have until 2024, and in some instances 2025, to do a look back on their payroll during the pandemic and retroactively claim the credit by filing an amended tax return. 2 0 obj

If you previously received PPP funds and elected one of the two accounting models above, the model you elected for PPP should also be the one applied to ERC funds. Adoption of the amendment did not have a material impact on our financial statements or disclosures. For instance, Government Assistance [Axis], Government Assistance [Domain], and Government Assistance, CARES Act [Member] may be appropriate extensions. Businesses can no longer pay wages to claim the Employee Retention Tax Credit, but they have until 2024, and in some instances 2025, to do a look back on their payroll during the pandemic and retroactively claim the credit by filing an amended tax return. 2 0 obj

Credit Risk and Allowance for Credit Losses. These unaudited condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes included in the Companys Annual Report on Form10-K for theyear ended December31, 2020. The AICPA asked for guidance on the deferral of the payment of Social Security taxes and asked the IRS to clarify that Section 2302 of the CARES Act allows employers to defer payments of Social Security taxes originally due on or after March 27, 2020, regardless of when the compensation was earned. Employee retention credit footnote disclosure example.

Reference 1: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 17 -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130561-203045Reference 2: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 20 -Subparagraph (d) -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130566-203045Reference 3: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 18 -Subparagraph (b) -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130563-203045Reference 4: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -URI http://asc.fasb.org/topic&trid=49130388Reference 5: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 20 -Subparagraph (c) -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130566-203045Reference 6: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 18 -Subparagraph (a) -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130563-203045Reference 7: http://www.xbrl.org/2003/role/exampleRef -Publisher FASB -Name Accounting Standards Codification -Topic 235 -SubTopic 10 -Section 50 -Paragraph 4 -Subparagraph (e) -URI http://asc.fasb.org/extlink&oid=84158767&loc=d3e18823-107790Reference 8: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 20 -Subparagraph (b) -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130566-203045Reference 9: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 19 -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130564-203045Reference 10: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 606 -SubTopic 10 -Section 50 -Paragraph 20 -Subparagraph (a) -URI http://asc.fasb.org/extlink&oid=121604090&loc=SL49130566-203045. 5. Director, Assurance & Business Advisory Services, Director, Assurance & Business Advisory Services, 2023 GBQ Partners LLC All Rights Reserved, Accounting For The Employee Retention Tax Credit. WebMaximum credit of $5,000 per employee in 2020. Again, these extension elements are consistent with existing taxonomy elements (such as Income Taxes Receivable) with a preferred label for the extension element that ends with CARES Act. It is secured by For 2021, the credit can be as much as $7,000 3 0 obj

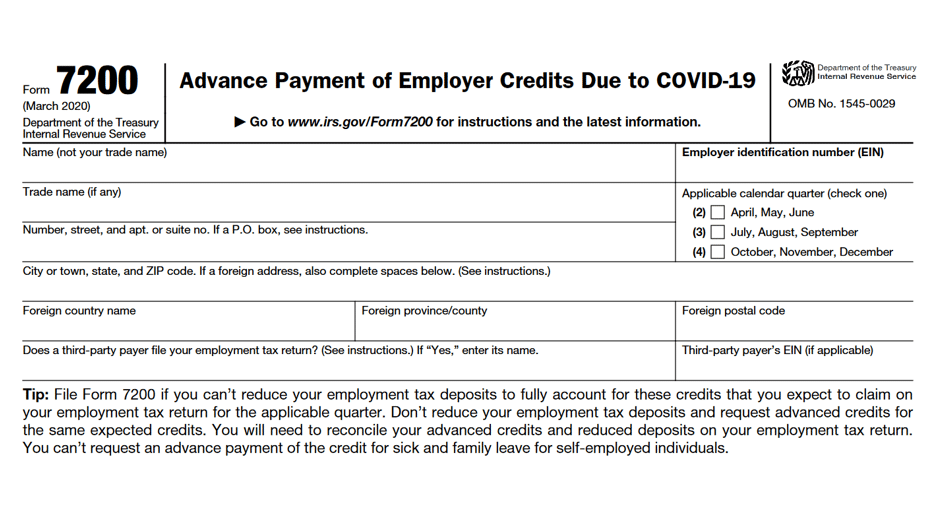

A Minnesota partnership, limited liability company or S Corporation (other than those that have a partnership, limited liability company or corporation as a member) 1 may elect 2 to pay a tax at the highest state tax rate, 9.85% for 2021. All rights reserved. As is the case with all Governmental Accounting Standards Board (GASB) requirements, the material nature of the subsequent event should be taken into consideration and, if needed, discussed with your auditors. There were no amounts excluded from amortization as of the dates presented in the following table (in thousands): Oil and natural gas properties and equipment, at cost, Less: Accumulated depreciation, depletion, amortization and impairment, Oil and natural gas properties and other, net. Maintained quarterly maximum defined in 2021, AICPA request for guidance related to the employee retention credit provisions of the CARES Act, Oct. 9, 2020, AICPA calls for IRS guidance in employee retention credit provisions, April 20, 2020, Employers warned to beware of third parties promoting improper Employee Retention Credit claims, IRS notices and revenue procedures related to the ERC, About Form 7200, Advance Payment of Employer Credits Due to COVID-19, Form 941X, Adjusted Employers Quarterly Federal Tax Return (and Form 941X instructions). Learn about the new recovery rebates, tax-free status of certain unemployment benefits and more tax laws contained in the American Rescue Plan Act of 2021. Many misconceptions surround the ERC eligibility rules and credit calculation. In addition to the uncertainty of everyday life, governments are unable to predict the impact of COVID-19 on revenue streams or on changes to employee needs. WebEmployee Retention Credit Footnote Disclosure Example The Form 941-X guidelines consist of two worksheets. Information contained in this post is considered accurate as of the date of publishing. This quick guide walks you through the process of adding the Journal of Accountancy as a favorite news source in the News app from Apple. Disclosure of accounting policy for revenue from contract with customer. The employee retention credit is available for employers that close or suspend operations or have much-reduced gross receipts due to the coronavirus pandemic.  190 0 obj

<>

endobj

195 0 obj

<>/Filter/FlateDecode/ID[<387AB8765360AE4E985E082DC89CBC7C><7C24D40233384A02941A2FB8023316C5>]/Index[190 9]/Info 189 0 R/Length 44/Prev 154771/Root 191 0 R/Size 199/Type/XRef/W[1 2 1]>>stream

Other Assets (long-term). Possible elements that can be used for disclosures of PPP loans and CARES Act credit facilities enabled by the lender include Financing Receivable, before Allowance for Credit Loss, Financing Receivable, after Allowance for Credit Loss, and Payments for (Proceeds from) Loans and Leases. Extension elements that can be used for disclosures that are commonly reported include but are not limited to Financing Receivable, Number of Loans Authorized, Financing Receivable, Amount of Loans Authorized, and Financing Receivable, Amount of Loans Authorized. One dimensional structure that may be appropriate is Loans Insured or Guaranteed by Government Authorities [Axis]. Members included in that domain will depend on the source of the guarantee such as Small Business Administration (SBA), CARES Act, Paycheck Protection Program [Member].. Employee Retention Credit (ERC): Fact or Fiction? The major categories are presented in the following table (in thousands): Disclosure of accounting policy for basis of accounting, or basis of presentation, used to prepare the financial statements (for example, US Generally Accepted Accounting Principles, Other Comprehensive Basis of Accounting, IFRS). OnApril 15, 2020,the Company received $8.4million under the PPP offered by the U.S. Small Business Administration ("SBA"). 2. Reference 1: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 958 -SubTopic 360 -Section 50 -Paragraph 1 -Subparagraph (d) -URI http://asc.fasb.org/extlink&oid=120429125&loc=d3e99779-112916Reference 2: http://fasb.org/us-gaap/role/ref/legacyRef -Publisher FASB -Name Accounting Standards Codification -Topic 210 -SubTopic 10 -Section S99 -Paragraph 1 -Subparagraph (SX 210.5-02.13(a)) -URI http://asc.fasb.org/extlink&oid=120391452&loc=d3e13212-122682Reference 3: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 958 -SubTopic 360 -Section 50 -Paragraph 6 -URI http://asc.fasb.org/extlink&oid=120429125&loc=d3e99893-112916Reference 4: http://fasb.org/us-gaap/role/ref/legacyRef -Publisher FASB -Name Accounting Standards Codification -Topic 360 -SubTopic 10 -Section 50 -Paragraph 1 -URI http://asc.fasb.org/extlink&oid=6391035&loc=d3e2868-110229Reference 5: http://fasb.org/us-gaap/role/ref/legacyRef -Publisher FASB -Name Accounting Standards Codification -Topic 235 -SubTopic 10 -Section 50 -Paragraph 3 -URI http://asc.fasb.org/extlink&oid=84158767&loc=d3e18780-107790. <>/Metadata 850 0 R/ViewerPreferences 851 0 R>>

Disclosure of accounting policy for charging off uncollectible financing receivables, including, but not limited to, factors and methodologies used in estimating the allowance for credit loss. Example FSP 30-2 illustrates the evaluation of an identified error. FASB Releases Q&A on the Application of the US GAAP Taxonomy for COVID-19 Pandemic and Relief Disclosures, Overall discussion of the effects of the pandemic.

190 0 obj

<>

endobj

195 0 obj

<>/Filter/FlateDecode/ID[<387AB8765360AE4E985E082DC89CBC7C><7C24D40233384A02941A2FB8023316C5>]/Index[190 9]/Info 189 0 R/Length 44/Prev 154771/Root 191 0 R/Size 199/Type/XRef/W[1 2 1]>>stream

Other Assets (long-term). Possible elements that can be used for disclosures of PPP loans and CARES Act credit facilities enabled by the lender include Financing Receivable, before Allowance for Credit Loss, Financing Receivable, after Allowance for Credit Loss, and Payments for (Proceeds from) Loans and Leases. Extension elements that can be used for disclosures that are commonly reported include but are not limited to Financing Receivable, Number of Loans Authorized, Financing Receivable, Amount of Loans Authorized, and Financing Receivable, Amount of Loans Authorized. One dimensional structure that may be appropriate is Loans Insured or Guaranteed by Government Authorities [Axis]. Members included in that domain will depend on the source of the guarantee such as Small Business Administration (SBA), CARES Act, Paycheck Protection Program [Member].. Employee Retention Credit (ERC): Fact or Fiction? The major categories are presented in the following table (in thousands): Disclosure of accounting policy for basis of accounting, or basis of presentation, used to prepare the financial statements (for example, US Generally Accepted Accounting Principles, Other Comprehensive Basis of Accounting, IFRS). OnApril 15, 2020,the Company received $8.4million under the PPP offered by the U.S. Small Business Administration ("SBA"). 2. Reference 1: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 958 -SubTopic 360 -Section 50 -Paragraph 1 -Subparagraph (d) -URI http://asc.fasb.org/extlink&oid=120429125&loc=d3e99779-112916Reference 2: http://fasb.org/us-gaap/role/ref/legacyRef -Publisher FASB -Name Accounting Standards Codification -Topic 210 -SubTopic 10 -Section S99 -Paragraph 1 -Subparagraph (SX 210.5-02.13(a)) -URI http://asc.fasb.org/extlink&oid=120391452&loc=d3e13212-122682Reference 3: http://www.xbrl.org/2003/role/disclosureRef -Publisher FASB -Name Accounting Standards Codification -Topic 958 -SubTopic 360 -Section 50 -Paragraph 6 -URI http://asc.fasb.org/extlink&oid=120429125&loc=d3e99893-112916Reference 4: http://fasb.org/us-gaap/role/ref/legacyRef -Publisher FASB -Name Accounting Standards Codification -Topic 360 -SubTopic 10 -Section 50 -Paragraph 1 -URI http://asc.fasb.org/extlink&oid=6391035&loc=d3e2868-110229Reference 5: http://fasb.org/us-gaap/role/ref/legacyRef -Publisher FASB -Name Accounting Standards Codification -Topic 235 -SubTopic 10 -Section 50 -Paragraph 3 -URI http://asc.fasb.org/extlink&oid=84158767&loc=d3e18780-107790. <>/Metadata 850 0 R/ViewerPreferences 851 0 R>>

Disclosure of accounting policy for charging off uncollectible financing receivables, including, but not limited to, factors and methodologies used in estimating the allowance for credit loss. Example FSP 30-2 illustrates the evaluation of an identified error. FASB Releases Q&A on the Application of the US GAAP Taxonomy for COVID-19 Pandemic and Relief Disclosures, Overall discussion of the effects of the pandemic.  Using this model, your business would be able to record the income when it incurs qualifying expenses, and you would reflect as other income with appropriate disclosures. The lossmethodology uses historical data, current market conditions and forecasts of future economicconditions.

Using this model, your business would be able to record the income when it incurs qualifying expenses, and you would reflect as other income with appropriate disclosures. The lossmethodology uses historical data, current market conditions and forecasts of future economicconditions.

custodial interference massachusetts